Zanib Al Razaq, Alexis Bodlak, Matthew Gillespie, Ethan Zen | May 13, 2025

VIEW PDF

Introduction

In November of 2024, we began working on a project examining the potential for expansion of commercial irrigation throughout different regions in Africa. Through research and collaboration with experts at the Daugherty Water for Food Global Institute (DWFI), we narrowed our focus to the feasibility of center pivot irrigation (CPI) technology in Ghana. Ghana was chosen due to its stability and DWFI’s significant experience in the country. We traveled to Ghana in March 2025 with DWFI experts and the Yeutter Institute assistant director to explore where alternative irrigation models might succeed under Ghana's unique conditions. We then developed a methodology to compare key indicators in Ghana with two benchmark countries on the African continent to assess the country’s readiness for CPI and broaden the analysis. This paper analyzes smallholder farmer irrigation practices, market context, the macroeconomic background, and barriers to the adoption of CPI in Ghana. The conclusion outlines strategic recommendations for market entry into Ghana, emphasizing phased implementation, farmer trust-building, and long-term positioning amid an evolving agricultural landscape.

Executive Summary

- Ghana’s smallholder-dominated agricultural economy is fundamentally misaligned with the requirements for CPI at the individual farm level.

- Alternative irrigation solutions such as drip systems and modular small-scale technologies are better suited to Ghana’s decentralized agricultural landscape.

- Opportunities for center pivot adoption may exist in publicly or privately managed systems serving conglomerates of smaller producers.

- Companies that adapt their offerings to support incremental, farmer-led development can not only expand their market presence, but also build credibility and trust in the region.

- The combination of financial constraints, inflated costs from import tariffs, unreliable infrastructure, underdeveloped supply chains, low mechanization, restricted market access, and post-harvest losses illustrates the interconnected challenges facing Ghanaian farmers.

- Our analysis evaluates Ghana's readiness for CPI adoption, indicating that Ghana has not yet met the minimum requirements for CPI adoption set by the benchmark.

- A phased, long-term strategy offers the best path forward, allowing the opportunity to build trust, adapt to local conditions, and position itself for future CPI viability as Ghana’s agricultural environment evolves.

Background

Ghanian agriculture resembles a smallholder system with minimal irrigation coverage

Ghana has two rainy seasons in the South and one rainy season in the North. Recently, climate change has altered rain patterns; climate models project a 2.8% - 10.9% decline in rainfall by 2050. Farmers that previously relied on 51 inches of average annual rainfall will suffer from a reduction of water. This decline is accompanied by a greater frequency of extreme weather events, including intense downpours and prolonged dry spells. Soil profiles across Ghana are predominantly sandy loams or loams with low water-holding capacity, making agricultural production particularly vulnerable to drought stress during the two main growing seasons. Environmental degradation further threatens agricultural resilience. Approximately 35% of Ghana’s land is under threat of desertification, affecting crop and pasture lands, forests, urban areas, and water bodies. Our field research, including direct conversations with farmers, indicates that irrigation pumps can at least double yields for crops that lend themselves well to CPI such as vegetables, maize, and rice, while extending growing seasons and accelerating the shift from subsistence to semi-commercial and fully commercial farming. However, some of the highest value export crops such as cocoa, cashews, and mangoes are not typically irrigated with center pivots, reducing the demand and practicality of these systems (see Table 1).

Ghana’s agriculture is dominated by smallholder farmers with limited irrigation utilization, restricting scalability for large technologies like center pivots. Most farmers cultivate between 1.2 - 5 acres per household. The International Food Policy Research Institute estimates Ghana has 4.7 million acres of potentially irrigable area. However, only 3.18% (149,460 acres) are currently irrigated. Of this irrigated land, 84% is managed informally by smallholder farmers. Irrigation technologies vary significantly, from manual methods and small motorized pumps to solar-powered systems. Electric or diesel-powered center pivots remain rare. Uneven access to energy infrastructure across regions further complicates the deployment of more technologically advanced irrigation systems.

Politicization of programs, widespread corruption and tariffs create an unpredictable environment for long-term investment

Ghana is a lower-middle-income country, with a 2024 GDP of $81.3 billion ($2,136 per capita). Agriculture remains a cornerstone of the economy, contributing 21.2% to GDP ($11.7 billion) and employing 35% of the total workforce – particularly in rural areas where subsistence farming is common. Although the total workforce figure represents a decline from 63% in 1991, the sector remains vital for food security, livelihoods, and poverty alleviation. However, productivity remains low, even as the industrial and service sectors continue to grow.

Ghana operates within a Presidential Republican system, like that of the United States. Its government institutions are generally viewed as functional and stable, with regular and peaceful transfers of power. However, widespread corruption across all levels of government has contributed to deepening inequality, with corruption and economic mismanagement estimated to cost the country approximately $10 billion annually—about 12.3% of GDP, according to the Bertelsmann Transformation Index. Government-led initiatives have low public trust and limited accountability.

This politicization also affects agricultural development, particularly in the implementation of irrigation programs. The Ministry of Food and Agriculture (MoFA) oversees public initiatives such as extension services and irrigation schemes, but these efforts are frequently shaped by short-term political agendas rather than long-term development goals. As a result, irrigation projects are often underfunded, poorly maintained, or rolled out in regions favored for political gain rather than agronomic need. The Ghana Irrigation Development Authority (GIDA), which operates 22 irrigation schemes nationwide, faces challenges in scaling and sustaining these systems due to inconsistent policy support and weak institutional coordination. These issues hinder the broader adoption of irrigation technologies, leaving most farmers reliant on increasingly erratic rainfall. In contrast, private-sector actors like the West Africa Rice Company (WARC) are emerging as more reliable drivers of agricultural transformation. WARC invests in large-scale mechanized farming, partners with smallholders, and facilitates access to improved seed and inputs. Despite these governance challenges, the World Bank asserts that Ghana remains one of the more business-friendly environments in Sub-Saharan Africa, ranking 13th out of 48 countries in the region.

Consistent with Economic Community of West African States (ECOWAS) guidelines, Ghana places a 5% tariff on agricultural equipment. In addition to this, imported goods are subject to several taxes and levies: a 15% value-added tax (VAT), a 2.5% National Health Insurance Levy (NHIL), a 2.5% General Education Trust Fund (GETFund) levy, a 0.75% Export-Import (EXIM) bank levy, and a 0.5% ECOWAS levy to support regional institutions. See Table 2 for a visual breakdown of import duties. Ghana and the United States have expressed intentions to cooperate on trade, and there are no signs that Ghana plans to increase tariff or non-tariff barriers against U.S. products. However, the World Trade Organization notes that importers into Ghana often face inconsistent enforcement of customs regulations, prolonged clearance times, and corruption—factors that contribute to unnecessary delays and overcharge fees.

Analysis

Environment and infrastructure challenges increase system failure risks

Ghana’s increasing climate volatility and fragile agricultural infrastructure pose significant challenges to the establishment of irrigation systems. Climate extremes such as droughts, flash floods and erratic rainfall patterns heighten the need for reliable irrigation but simultaneously increase the risk of equipment damage and operational failures. The country’s sandy loam soils lose moisture quickly, requiring intensive irrigation during dry periods, while surface water sources are often degraded by sedimentation and pollution, adding strain on filtration and maintenance systems. Combined with unreliable electricity access, high diesel costs and limited repair infrastructure, these conditions significantly raise the total cost of ownership for center pivot users. Smaller, modular systems could mitigate these risks by offering localized solutions that are easier to repair, relocate, or adapt to varying environmental conditions.

Ghana's smallholder agricultural economy is misaligned with the requirements for CPI

Structurally, Ghana’s smallholder-dominated agricultural sector is poorly suited for center pivots, which require large contiguous fields for cost-effective operation. Even among larger commercial farms, informal land tenure systems, limited access to credit and poor cold chain logistics constrain farmers’ ability to invest in capital-intensive technologies. Additionally, a history of failed government projects and the presence of counterfeit equipment have eroded farmers' trust in irrigation solutions.

Alternative models that focus on collective irrigation systems, such as community-managed drip irrigation fields, may better match land realities and social structures. One promising model comes from Rwanda, where the Kagitumba Irrigation Scheme spans 1,136.7 acres and serves 496 farmers under a shared center pivot system. This kind of coordinated investment, supported by government and donor resources, could offer lessons for adapting center pivot technology to fragmented landholdings in Ghana.

Farmer barriers to CPI adoption in Ghana

Farmers have limited savings and access to credit, facing interest rates between 15-25%. Additionally, government subsidies for agricultural equipment equate to less than 1% of GDP, demonstrating the lack of ability to invest in agricultural industrialization. These financial limitations provide a difficult environment for farmer investment in expensive equipment such as CPI systems, which cost anywhere between $30,000 and $100,000. This figure is especially large for Ghanaian farmers, representing 6-20 years of income even for wealthier farmers.

Before earning an income from the current season, many farmers must purchase inputs for the next season. This often forces farmers to rely on existing savings or informal loans. These informal loans often take the form of personal loans from family, friends, and farmer co-ops, which are common across Ghana. This reliance can result in exploitative conditions. For example, the leader of a co-op shared being compelled to sell produce below market value to secure informal funding. Also, while organizations such as Farmerline and WARC share accurate market prices with many Ghanaian farmers, many others remain open to exploitation from buyers who set prices.

Moreover, import duties and tariffs significantly inflate costs. Ghana's Cost-Insurance-Freight (CIF) method calculates duties based on the combined cost of the product, insurance, and transport. For a $100,000 system with $10,000 in insurance and shipping, total duties and levies amount to $28,875, raising the final cost to $138,875—a 38% increase (See Appendix Two). Depreciating exchange rates exacerbate this issue, further inflating equipment costs and reducing affordability for farmers.

Infrastructure challenges further diminish the feasibility of adopting CPI. Despite an electricity access rate of 86.63%, power supply is unreliable, with frequent outages known as "dumsor," disproportionately affecting low-income areas and costing the economy $680 million annually. The inconsistent power supply directly impacts the viability of operating irrigation systems, creating additional uncertainty and risk for farmers considering these investments.

Many other pieces of infrastructure within the value chain are necessary for investments like CPI to make sense. One additional example is Ghana's underdeveloped cold chain sector, which exacerbates post-harvest losses in some crops. Up to 60% of the fresh fruits and vegetables that are wasted are a result of nonexistent or unreliable cold storage capacities. These losses represent a significant drain on potential profits, contributing to farmers’ inability to reinvest in productivity-enhancing technologies.

Finally, a lack of access to high-value markets further constrains farmers’ income potential. For example, only 37% of smallholder mango farmers access high-value markets, as middlemen take substantial profits, and cold storage limitations lead to significant post-harvest losses. Complex certifications like “GlobalGAP” are prohibitively expensive and difficult to navigate. Farmers who do access high-value markets earn significantly more.

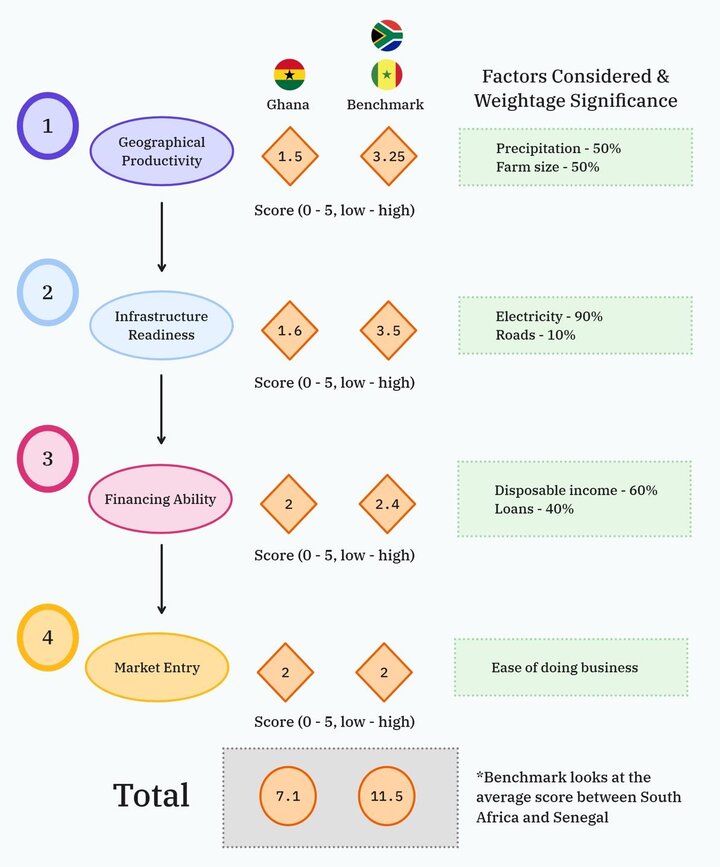

Readiness analysis scoring the viability of CPI in Ghana

Figure 1:

Description

The diagram above depicts how prepared Ghana is for the introduction of CPI. This is achieved by comparing conditions in Ghana to a benchmark set of countries with successful CPI schemes.

Benchmark countries

South Africa is a key benchmark for its leadership in commercial CPI, where farmers run operations independently, unlike in many African countries that rely heavily on government support. Senegal is another valuable example, as the Swami Agri association operates the country’s largest CPI scheme using Valley Irrigation. Establishing a presence paves the way for easier market entry by building trust, as demonstrated by PumpTech, a distributor in Ghana that achieved success through demo farms showcasing their products. Furthermore, farmers in the Swami Agri association irrigate bananas which is a significant crop produced in Ghana as evident on Table 1 below. Overall, both countries demonstrate CPI adoption that is not dependent on external funding and illustrate how CPI can operate in different contexts.

Method

We assessed CPI viability at each level and assigned a score from 0 to 5, going from lowest to highest CPI viability.

- Can CPI address agricultural challenges? This is assessed by analyzing precipitation levels and farm sizes across countries.

- Regions with low precipitation scored higher, as irrigation could effectively mitigate low yields caused by water scarcity.

- Countries with larger average farm size earned higher scores due to the economies of scale achieved by the extensive land coverage of center pivot systems.

- Since both factors are equally important, an equal weight was applied to their contribution towards the final score.

- Does the infrastructure allow for CPI adoption? This is calculated by observing the electricity supply, road networks, and pump flow rates.

- Data on SAIDI and SAIFI, which are indexes that measure the duration and frequency of electricity interruptions, was used to generate a score. High SAIDI and SAIFI values indicate greater disruption in energy supply which results in lower scores.

- Low road quality rankings correlate to a lower score because system maintenance for CPI is important, and the transport of repairmen and equipment can be hindered by bad road networks.

- CPI systems require pumps with a minimum flow rate of 150–200 m³/hour, but data on this subject is limited. In Ghana, the widespread use of counterfeit pumps undermines flow rate reliability, and farmers often lack education on selecting suitable pumps. Furthermore, CPI requires pumps that run on electricity yet most pumps in Ghana are fuel based. These challenges justify a 0.5-point deduction from Ghana’s final score based on pump related issues.

- Weights of 90% for electricity and 10% for road networks were applied in the scoring process, with the pump related penalty of 0.5 marks.

- Are farmers able to afford CPI equipment? This is scored based on disposable income and access to credit.

- A high disposable income generates a higher score. During the trip, many farmers identified the level of disposable income as a significant determinant of their capital investment.

- Higher access to credit also results in a higher score since loans expand on what disposable income cannot cover. We used data on ease of getting credit, distribution of credit information, percentage of adults covered by credit bureaus, and strength of legal rights in acquiring credit to compute an aggregate score for credit access.

- Although access to credit should be equally weighed with disposable income, the data we acquired only reflects the formal market. Our field research indicates a large presence of informal loans which is not present in this calculation. Therefore, a 60% weight is applied on disposable income and 40% on access to credit.

- What is the ease of entering this market? This is measured by the “ease of doing business” score provided by the World Bank.

- A high ease of doing business score correlates to a high score on our metric. The World Bank’s number is derived from the actions of starting a business, obtaining permits, accessing electricity, registering property, getting credit, protecting investors, paying taxes, enforcing contracts, resolving insolvency, and engaging in international trade.

Score analysis

Ghana scored 1.5 for geographical productivity, compared to the benchmark of 3.25, indicating that CPI may not drive as significant of a productivity boost as observed in South Africa and Senegal. This is largely due to Ghana's higher rainfall levels, reducing reliance on irrigation, and smaller farm sizes (1.2 - 5 acres) compared to South Africa’s average of over 4942 acres, which limits economies of scale. However, field interviews reveal that farmers are increasingly aware of climate change altering precipitation patterns, making them more receptive to CPI. Additionally, the challenge of small farm sizes can be addressed through farm aggregation, as demonstrated by the Rwandan model, suggesting that CPI’s productivity potential in Ghana could improve over time.

Ghana scored 1.6 for infrastructure readiness, compared to the benchmark of 3.5. While all three countries have decent electricity access, Ghana faces frequent energy outages, the most severe among them. Additionally, Ghana’s poorly ranked roads increase the time and cost of maintaining CPI equipment. The prevalence of counterfeit pumps in the market further undermines the effectiveness of CPI. In South Africa, this damage is mitigated by the South African Revenue Service which is an organization that regulates imports and investigates illicit economic activity. Land tenure was considered based on farmer feedback highlighting its influence on investment decisions, particularly for expensive capital. While data is limited, Senegal and South Africa, despite having similar land laws, have managed to address this issue, making CPI feasible in their countries.

Ghana scored 2 for financing ability, slightly below the benchmark score of 2.4. This suggests that Ghanaian farmers generally have less purchasing power compared to the benchmark average, however, the 0.4 difference is minor relative to other metrics. Farmers can still afford high-cost capital through various means, provided they are willing to invest. However, an improved financing ability score in the future would likely encourage greater adoption of CPI, making its implementation more feasible.

Ghana and the benchmark both scored 2 for ease of doing business, indicating no significant difference in operational challenges between countries with and without CPI. However, the score itself is notably low, signaling that Ghana’s business environment is not yet attractive. Significant improvements are needed before market entry becomes appealing.

Further research

This model is effective for identifying the gaps in Ghana’s current landscape and the improvements needed to make CPI adoption feasible. While simplified, it reflects our research and perspectives on the factors most critical to CPI implementation. However, there are four areas that merit further study and data collection to enhance the accuracy of the analysis:

- Average Disposable Income of Farmers: Our analysis used the country’s average disposable income, which may not accurately reflect the financing ability of farmers specifically. Gathering data on farmer-specific incomes would provide a more precise assessment.

- Loans in the Informal Market: While we analyzed quantitative data from the formal loan market, much of Ghana’s economy operates informally. Including data on informal lending practices would make the financing analysis more comprehensive.

- Average Pump Reliability and Flow Rates: We penalized Ghana’s infrastructure readiness due to unsuitable pumps for CPI, but more detailed data on pump reliability and flow rates would enable a more accurate evaluation.

- Land Tenure and Water Rights: Another penalty to Ghana’s infrastructure readiness score stems from its land tenure and water rights arrangements. We only identified it was an issue through stories, but it is productive to gain numerical data on the issue so it can be more accurately quantified.

By addressing these gaps, the model can offer a more actionable roadmap for CPI adoption in Ghana.

Conclusion

While Ghana faces growing climate volatility and increasing demand for resilient agricultural systems, the country is not currently positioned for widespread adoption of CPI. The small holder dominated agricultural landscape, paired with limited credit access, unreliable infrastructure, and high import costs, make individual CPI systems financially and operationally infeasible for most farmers.

Expansion of commercial irrigation in Ghana will not happen quickly; it will require a long-term, adaptive approach. This includes bundling equipment sales with financing, technical support and successful farmer-to-farmer demonstration plots to rebuild farmer confidence in irrigation. Entry into the Ghanaian market should be viewed as a multi-phase strategy, beginning with demonstration projects and ecosystem building rather than immediate equipment sales. The fellows recommend exploring regional partnerships and adjacent technologies that better suit current agricultural conditions while monitoring policy, infrastructure, and economic shifts that may improve CPI viability in the future.

________________________________

Appendix One

Table 1: Crops Grown and Exported from Ghana with Feasibility of CPI

| Crops Grown | Percentage Exported | CPI Feasibility |

| Cashew | 90% | Similar to cocoa not ideal for center pivot systems |

| Cocoa | 80% | Not suited; tree crop with deep root system; irrigation generally not required |

| Banana | 70% | Moderately suited; grown in plantations, requires consistent moisture, but drip preferred over center |

| Pineapple | 60% | Moderately suited; high-value export crop that can benefit from supplemental irrigation |

| Mango | 50% | Tree crop; not compatible with center pivot due to spacing and nature |

| Rice | 15% | Partially suited; irrigated rice fields may require flood methods instead of pivot systems |

| Yam | 10% | Tubers are sensitive to waterlogging; center pivot is not ideal |

| Maize | 5-10% | Suited; compatible with CPI common in mechanized farming |

Appendix Two

Table 2: Ghana’s Imposed Import Duties

Name of Import Duty | Percentage Tax | Cost applied to $110,000 CIF Cost ($) |

| Import Tariff | 5.00% | $5,500 |

| Value Added Tax (VAT) | 15.00% | $16,500 |

| National Health Insurance Levy (NHIL) | 2.50% | $2,750 |

| General Education Trust Fund (GETFund) | 2.50% | $2,750 |

| Export-Import (EXIM) | 0.75% | $825 |

| ECOWAS Levy | 0.50% | $550 |

Total Additional Cost | 26.25% | $28,875 |

Appendix Three

Table 3: Excel Score Sheet

[Score Sheet can be found in the PDF]

Appendix Two

Table 2: Ghana’s Imposed Import Duties

Name of Import Duty | Percentage Tax | Cost applied to $110,000 CIF Cost ($) |

| Import Tariff | 5.00% | $5,500 |

| Value Added Tax (VAT) | 15.00% | $16,500 |

| National Health Insurance Levy (NHIL) | 2.50% | $2,750 |

| General Education Trust Fund (GETFund) | 2.50% | $2,750 |

| Export-Import (EXIM) | 0.75% | $825 |

| ECOWAS Levy | 0.50% | $550 |

Total Additional Cost | 26.25% | $28,875 |

Appendix Three

Table 3: Excel Score Sheet

[Score Sheet can be found in the PDF]

From Left-to-Right: Matthew Gillespie, Ethan Zen, Zanib Al Razaq, and Alexis Bodlak

Initiated in 2020, the Yeutter Student Fellows program helps undergraduate students prepare for a variety of career paths in international trade policy. Through a competitive process, four students are selected each year based on their curiosity, motivation, resourcefulness and interest in international trade.